The Vast Wealth of the LDS Church, the Doctrine of Tithing, and the Biblical Mandate of Stewardship

Introduction: The Widow’s Mite and the World’s Richest Church

Imagine a widow in rural Mexico. She is a faithful Latter-day Saint, a convert of ten years. She earns the equivalent of $3.50 a day making tortillas. She has been taught since her baptism that tithing is not optional — that the temple recommend she must possess to see her daughter married will be withheld if she does not pay a full ten percent of her income to the Church. And so, every week, she faithfully drops thirty-five cents into the envelope, seals it, and hands it to her ward clerk. It is not a lot. But in the language of the Savior, it may be her all.

Imagine a widow in rural Mexico. She is a faithful Latter-day Saint, a convert of ten years. She earns the equivalent of $3.50 a day making tortillas. She has been taught since her baptism that tithing is not optional — that the temple recommend she must possess to see her daughter married will be withheld if she does not pay a full ten percent of her income to the Church. And so, every week, she faithfully drops thirty-five cents into the envelope, seals it, and hands it to her ward clerk. It is not a lot. But in the language of the Savior, it may be her all.

Now consider this: as of 2024, that woman’s thirty-five cents flows — along with an estimated $28 billion in annual contributions from 17.5 million members worldwide — into one of the most extraordinary financial machines in human history. The Church of Jesus Christ of Latter-day Saints, headquartered in Salt Lake City, Utah, has accumulated an estimated total wealth of $293 billion. Its total investment reserves — including equities, real estate, private holdings, and cash — are estimated at approximately $206 billion, managed by a secretive firm called Ensign Peak Advisors. Of that sum, Ensign Peak’s publicly disclosed equity portfolio alone, as reported in SEC filings, exceeds $56 billion. According to an independent analysis by The Widow’s Mite Report — a name borrowed from the very Gospel passage that comes to mind when imagining that Mexican widow — the Church’s investment returns now exceed its global operating costs. The machine, in other words, has achieved escape velocity.

“As an endowment, invested reserves are sufficient to fund church programs forever, even if donations stopped completely.” — The Widow’s Mite Report, 2024 Year-End Analysis (thewidowsmite.org), cited in The Salt Lake Tribune, April 1, 2025

This essay is not a polemic. It is not an attack on the sincerity of Latter-day Saints, many of whom demonstrate extraordinary personal generosity, community devotion, and spiritual earnestness. Rather, it is an attempt — from the standpoint of a traditional Christian theologian — to ask the questions the widow deserves to have asked on her behalf. What does the Bible actually teach about the relationship between a religious institution and its financial resources? What are the obligations of stewardship when a church grows so wealthy it no longer needs the gifts of its poorest members — yet continues to collect them? And what does it mean for the integrity of religious leadership when financial opacity and institutional self-preservation begin to shadow the cause of their version of the truth?

The answers we will find are both historically illuminating and theologically urgent.

Section One: From Poverty to Empire — The Historical Arc of LDS Finances

Origins in Scarcity: The Economic Vision of Joseph Smith

The Church of Jesus Christ of Latter-day Saints was born in 1830 amid religious ferment, frontier poverty, and utopian economic aspirations. Joseph Smith’s early theological vision was explicitly communitarian. The Law of Consecration, revealed in the Doctrine and Covenants, called on the early Saints to deed all their property to the Bishop of the Church, receive back what they needed for their family’s “stewardship,” and contribute any surplus to a common storehouse for the benefit of the poor. It was, in its idealized form, a kind of sacred communalism grounded in the theology of Zion — a heaven-on-earth society in which no one would be rich, and no one would be poor.

In practice, the Law of Consecration proved administratively unworkable. Voluntary compliance was inconsistent, legal title arrangements were contested, and internal tensions over property created more conflict than unity. The system largely collapsed in the early 1830s, well before the Saints were expelled from Missouri in 1838 and later driven from Nauvoo, Illinois, in 1846. A modified version — the United Order — was attempted again under Brigham Young in Utah during the 1870s, with cooperative communities established in towns such as St. George and Orderville. These too ultimately dissolved, unable to survive the pressures of a growing, increasingly diverse membership and the encroaching market economy of the American West.

What endured was tithing. Though practiced informally from the Church’s earliest years, tithing was formalized by revelation in 1838 and became the Church’s primary financial mechanism during the Utah territorial period under Brigham Young’s direction. Where the Law of Consecration had asked for everything, tithing asked a manageable ten percent of one’s increase. It was a theological adjustment rooted in practical necessity — one that would, over the course of a century and a half, quietly accumulate into one of the largest religious fortunes in human history.

Contemporary LDS commentators have largely absorbed the failure of the Law of Consecration into a framework of theological continuity, presenting its collapse not as an institutional failure but as a deferral — a higher law awaiting a more spiritually prepared people. One representative treatment, published on a Latter-day Saint temple covenant blog, draws on BYU Professor Steven C. Harper’s observation that “the choice not to live the law of consecration does not end the law of consecration” — comparing the collapse of the United Order to NASA ceasing operations without nullifying the laws of rocket propulsion. The analogy is rhetorically elegant. It is also, on examination, precisely backward. NASA’s cessation does not affect physical laws because those laws are not contingent on human institutions. The Law of Consecration, by contrast, was an institutional covenant — one that required a functioning community of voluntary participants to exist at all. When the institution collapsed under the weight of “personal greed, persecution, and other extenuating circumstances” (the author’s own words), the law did not float free of its failure. It failed with it.

What this kind of apologetic framing accomplishes — often quite skillfully — is the redefinition of a concrete historical and institutional collapse as a spiritual aspiration still nobly in force. The Law of Consecration becomes not something the Church tried and abandoned, but something it is perpetually becoming. In that reframing, the $206 billion reserve at Ensign Peak is presumably a form of consecration in progress — assets dedicated to building up the kingdom, awaiting the right moment for distribution. The widow’s thirty-five cents, it turns out, was never really lost. It was invested. The question the reframing cannot answer is the one Scripture keeps asking: For whom? By whose accounting? And who gets to know?

But there is a deeper problem the apologetic framing cannot paper over — one that cuts to the foundation of LDS prophetic authority itself. The Law of Consecration was not presented by Joseph Smith as a pastoral suggestion, a pious aspiration, or a community experiment. It was presented as a divine revelation — the direct word of God to His restored Church through His chosen prophet. Section 42 of the Doctrine and Covenants, where the law is established, carries the weight of Thus-saith-the-Lord language that admits no ambiguity: this was God’s will, communicated through revelation, binding upon the covenant community.

If that is true, then the law’s collapse is not a minor administrative inconvenience. It is a catastrophic theological problem. A God who issues binding revelations that prove “administratively unworkable” within a few years — abandoned not because the Saints transcended them, but because human greed, legal conflict, and institutional dysfunction made them impossible to sustain — is either a God whose revelations are contingent on human cooperation in ways that strain the very definition of revelation, or a prophet whose “Thus saith the Lord” reflected something other than divine communication.

It will be said, as it is always said when prophetic promises collapse under the weight of human failure, that the problem lay with the people, not the prophecy — that the Saints failed the revelation, and not the other way around. But this defense, while theologically tidy, is available to explain the failure of virtually any prophetic claim whatsoever. If every unfulfilled “revelation” can be attributed to the insufficiency of the people who received it, the concept of prophetic revelation loses its falsifiability — and therefore its meaning. A standard that can never be tested cannot be trusted.

The Law of Consecration sits alongside other significant unfulfillments in the early prophetic record: Joseph Smith’s 1832 prophecy that a temple would be built in Independence, Missouri, in his own generation (D&C 84:4-5) — a temple that has never been built; his 1835 declaration that the Lord’s return was “nigh, even fifty-six years should wind up the scene” (History of the Church 2:182); and others that LDS apologists have spent considerable energy reinterpreting, contextualizing, or quietly setting aside. The pattern is consistent enough to raise a question that faithful engagement cannot responsibly avoid: at what point does a repeated pattern of prophetic non-fulfillment constitute not a testimony of human weakness, but evidence that the prophetic office itself was something other than what it claimed to be?

The widow in rural Mexico deserves that question to be asked on her behalf — not as an act of contempt for her faith, but as an act of respect for her intelligence and her eternity.

Near-Ruin: The Financial Crisis of the 1880s and 1890s

The financial history of the Church of Jesus Christ of Latter-day Saints is not a simple story of unbroken prosperity. In the 1880s and 1890s, the Church faced genuine catastrophe. The Edmunds-Tucker Act of 1887 — federal anti-polygamy legislation — disincorporated the Church and directed the confiscation of all Church property valued over $50,000. The U.S. Supreme Court upheld the law in May 1890, in Late Corporation of the Church of Jesus Christ of Latter-day Saints v. United States, authorizing the federal government to seize Church assets and hold them in receivership. The financial damage was compounding: internal records later revealed that the Church’s total liabilities exceeded its active assets by more than $1.3 million — a clear case of technical insolvency. The Panic of 1893 deepened the crisis further.

The LDS Church fell into severe financial distress due to several factors that were exacerbated by the nationwide economic depression that began with the Panic of 1893. Under the provisions of the anti-polygamy Edmunds–Tucker Act of 1887… the U.S. government had confiscated church property, including tithing money donated by members. — Wikipedia, “Finances of the Church of Jesus Christ of Latter-day Saints“

The rescue came through two channels. First, under President Lorenzo Snow, who took office in 1898, the Church issued a $1 million bond to fund its indebtedness — backed not by Kuhn, Loeb & Co., as is sometimes claimed in popular accounts, but by Church financial trustees. Second, and far more consequentially, Snow launched an intensive and spiritually charged campaign to revive tithing compliance. In May 1899, while visiting the drought-stricken settlement of St. George, Utah, Snow received what he described as a divine manifestation and delivered a landmark two-day address declaring that the Lord required the Saints to pay a full tithe. The timing was, one might observe, providential in the most convenient sense of the word — a revelation whose content happened to be precisely what a financially insolvent institution most urgently needed to hear. His promise — that faithfulness in tithing would open the windows of heaven — was not merely a theological exhortation. It was a financial strategy born of institutional desperation. That the heavens, once opened, would pour their blessings into a $206 billion investment reserve rather than the storehouses of the poor is a detail the St. George address did not anticipate.

It worked. Tithing revenues surged across the Church. By April 1907, President Joseph F. Smith stood before the General Conference and announced that the Church “owes not a dollar that it cannot pay at once.” The bonded indebtedness had been retired in full.

This historical context is critical for understanding what follows. The aggressive culture of tithing compliance that crystallized in the early twentieth century was forged in the furnace of near-bankruptcy. What began as a survival mechanism — a desperate appeal to covenant loyalty in the shadow of federal confiscation and financial ruin — became institutional doctrine. Over the next century and a quarter, it would quietly generate an accumulation of wealth the Church’s founders could never have imagined.

From Recovery to Empire: The Twentieth Century

With debt retired and tithing revenues flowing steadily, the Church embarked on a century of careful, diversified accumulation. It acquired vast landholdings across the American West, established agricultural operations, built an expanding real estate portfolio, and founded or acquired numerous commercial enterprises. Churches in the United States are automatically exempt from federal income tax under the Internal Revenue Code — an exemption that predates the formal 501(c)(3) designation established by Congress in 1954. The LDS Church’s tax-exempt status, effectively in place throughout the twentieth century, sheltered its growing income and investment returns from federal taxation, allowing capital to compound largely undisturbed.

From 1915 to 1959, the Church disclosed detailed financial statements at its annual April General Conference. These reports, read aloud to assembled members, itemized both income and expenditures by category — a form of institutional accountability that, for over four decades, gave tithe-payers a genuine window into how their contributions were used. Then that window closed.

In 1959, the Church posted an extraordinary deficit of $8 million — a dramatic reversal from a $7 million surplus the prior year. Shortly afterward, Henry Moyle, appointed as Second Counselor to President David O. McKay in June 1959, assumed oversight of Church finances and immediately abandoned the existing budget. His reasoning was expansionist: by constructing larger meetinghouses ahead of projected growth, the Church would attract converts to fill them. The accelerated building program plunged the Church into cascading deficits, reaching a reported $32 million shortfall by 1962. As the scope of the overspending became undeniable, Moyle persuaded President McKay not to publish even an abbreviated accounting of Church expenditures. Financial transparency, which had been a hallmark of LDS institutional accountability for more than four decades, ended at the precise moment it became most inconvenient. McKay eventually relieved Moyle of his administrative responsibilities, and spending was reined in, but the financial disclosures were never restored.

The Church has not released full financial statements to its American membership since. It discloses finances in the United Kingdom, Canada, and Australia, where law requires it, but members in the United States — who provide the largest share of contributions — receive only a brief annual certification from an internal Auditing Department confirming that funds are being spent “in accordance with the purposes and doctrines of the Church.” What those purposes are, in what proportion, and to what ends, remains entirely undisclosed. No independent auditor has reviewed the books. No line items are published. The institutional silence that Henry Moyle initiated in 1960 has now lasted more than six decades.

Zion, Incorporated: 1907–1960

The years between 1907 and 1960 are not a footnote in LDS financial history. They are the foundation on which everything that followed was built.

With its debts retired and its tithing culture newly galvanized, the Church under President Heber J. Grant — who served from 1918 to 1945, the longest presidency in modern Church history — began the deliberate construction of a commercial and institutional empire. Grant, himself a former banker and businessman, understood that institutional survival required more than tithing revenue. Under his leadership, the Church acquired or expanded its holdings in banking, insurance, and agriculture, and consolidated control over Zion’s Cooperative Mercantile Institution (ZCMI). This Church-founded department store had operated since Brigham Young’s era. The theological vision of Zion — the communal society in which no one would be rich and no one poor — was quietly giving way to something more recognizable: a vertically integrated religious corporation.

The Great Depression tested the model but ultimately strengthened it. In 1936, under Grant’s direction, the Church launched its formal welfare program — a network of storehouses, farms, and canneries designed to provide for members without recourse to federal relief. It was genuinely admirable, and it became one of the most effective pieces of institutional public relations in American religious history, casting the Church as a model of self-reliant communal care at the precise moment that image was most valuable. It also, not incidentally, kept tithing-paying members invested in an institution that visibly served them.

The postwar decades brought explosive growth on every front. Under President David O. McKay, who served from 1951 to 1970, Church membership surged past two million and then toward three, carried forward by an aggressive global missionary program and the broader postwar religious revival that defined American cultural life in the 1950s. New meetinghouses rose across the United States and around the world. The Church’s media holdings expanded — Bonneville International took shape as a broadcasting operation of genuine commercial scale. Agricultural acquisitions accumulated quietly across the American West and, eventually, internationally.

By the late 1950s, the Church that had entered the century technically insolvent had become something its founders and even its early twentieth-century leaders could not have fully anticipated: a diversified economic institution of substantial size, generating revenue streams well beyond the tithing envelopes of its members. The annual financial reports, still being read at General Conference, reflected real prosperity. And then, in 1960, as Henry Moyle’s accelerated building program tipped the ledger back into deficit, the reports stopped. The membership that had watched the Church climb from bankruptcy to abundance was told, in effect, that the financial story was no longer theirs to follow. The windows of heaven, it seemed, had developed a privacy setting.

Ensign Peak: The $206 Billion Secret

The most dramatic chapter in the LDS Church’s impressive financial history began with the quiet creation of Ensign Peak Advisors, a Salt Lake City–based investment management firm wholly owned and operated by the Church. For more than two decades, Ensign Peak functioned in near-total obscurity. Its offices were located above a food court in downtown Salt Lake City, with no signage in the building lobby identifying the firm. Employees were required to sign lifetime confidentiality agreements, and most staff were not told the total value of the assets they managed — a deliberate compartmentalization that ensured no single employee could grasp, or disclose, the full picture. The firm did not appear in Church directories, was not referenced in General Conference addresses, and was unknown to the overwhelming majority of the 17.5 million tithe-paying members whose contributions had seeded its growth. It maintained no public-facing website, issued no press releases, and sought no profile. When portfolio managers attended investment conferences, they were instructed to identify themselves as working for a “family office” rather than disclose their employer. Over time, the firm built a massive portfolio encompassing publicly traded equities, bonds, private equity interests, and other instruments — and the method by which it kept that portfolio hidden was not merely cultural discretion but structured legal architecture: a network of shell LLCs, each filing its own SEC disclosures under a name that revealed nothing, collectively obscuring the fact that a single religious institution had quietly assembled one of the largest investment funds in the world.

In the secular financial world, this profile — anonymous ownership, compartmentalized employees, shell-company filings, a “family office” cover identity, and a portfolio growing into the tens of billions — would have drawn regulatory scrutiny long before two decades had elapsed. Hedge funds managing a fraction of Ensign Peak’s assets operate under layers of SEC oversight, investor disclosure requirements, and audit obligations that leave little room for the kind of structural concealment Ensign Peak sustained for over twenty years. That it took a whistleblower, rather than a regulator, to finally expose the arrangement speaks not only to the institutional audacity of the scheme, but to the singular legal shelter that religious designation provides in the United States — a shelter that, in this case, functioned less as a protection of religious liberty than as a shield for financial opacity on a breathtaking scale.

Latter-day Saint officials kept the size of the church’s $100 billion investment reserves secret for fear that public knowledge of the fund’s wealth might discourage members from paying tithing, according to the top executive who oversees the account. — The Salt Lake Tribune, February 8, 2020

Between 1997 and 2019, rather than filing required SEC Form 13F disclosures in its own name, Ensign Peak created a network of more than a dozen shell companies — structured as LLCs (limited liability companies) — and filed the required disclosures in their names instead. The choice of LLC structure was not incidental. Unlike S corporations, LLCs carry far fewer mandatory financial reporting and governance requirements, making them well-suited as vehicles for obscuring ownership, control, and the true scale of accumulated assets. The scheme was nonetheless elaborate in its execution: Church-employed designees signed filings attesting that each shell company had independent investment authority over its portfolio — a claim the SEC later found to be materially false. Each LLC existed on paper as a discrete investment manager, but all roads led back to Ensign Peak, and through Ensign Peak, to the Church. The purpose, according to the SEC’s own order, was to “avoid disclosure of the amount and nature” of the Church’s assets — a goal the structure achieved for more than two decades before a whistleblower finally brought it to light.

The man who oversaw this operation was Roger Clarke, Ensign Peak’s managing director. In a 2020 interview with the Wall Street Journal, Clarke acknowledged that the portfolio had been concealed specifically out of concern that knowledge of the Church’s vast wealth would cause members to reduce their tithing contributions. That admission — made by the head of one of the largest investment funds on earth — is among the most consequential statements ever made by a senior LDS financial official. It reveals an institutional calculus in which the spiritual covenant of tithing was deliberately subordinated to the financial imperative of maintaining donation flow. Members were not told because telling them might cost the institution money.

The secret did not hold. In November 2019, David Nielsen — a former senior portfolio manager at Ensign Peak who had left Wall Street specifically to serve his church — filed a whistleblower complaint with the IRS alleging that Ensign Peak had accumulated approximately $100 billion in assets and was operating more as a for-profit hedge fund than a tax-exempt charitable organization. His brother Lars provided the documents to the Washington Post, and the story ignited a global conversation about the relationship between LDS theology and LDS finance. Significantly, Ensign Peak quietly began filing 13F disclosures in its own name almost immediately after learning of the complaint.

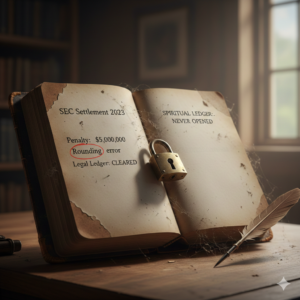

In February 2023, the SEC formalized what the whistleblower had alleged. It charged both Ensign Peak Advisors and the Church with failing to properly disclose the investment portfolio through fraudulent shell company filings spanning more than two decades. To settle the charges — without admitting wrongdoing — Ensign Peak agreed to pay a $4 million penalty, and the Church agreed to pay $1 million, for a combined total of $5 million. Critics observed that the penalty was trivially small relative to the scale of the concealment, but it constituted an official finding by U.S. federal regulators of deliberate financial deception.

By the close of 2024, The Widow’s Mite Report estimated the Church’s total investment reserves — including non-publicly disclosed assets — had reached approximately $206 billion, having gained an estimated $23.5 billion in a single year. Total Church wealth, incorporating operating assets such as temples, meetinghouses, farmland, the BYU university system, and global real estate holdings, is estimated at $293 billion. Independent projections suggest that if current growth trajectories continue, the Church could approach $1 trillion in total wealth within two decades.

LDS Church could be a $1 trillion denomination by 2044, report suggests. — The Christian Post

By virtually any measure, the Church of Jesus Christ of Latter-day Saints is the wealthiest religious institution in the United States and among the wealthiest on earth — a position achieved in large part through a culture of tithing compliance forged in the nineteenth century and an investment operation that functioned, for more than twenty years, in deliberate concealment from both its members and federal regulators. The SEC settlement of 2023 addressed the legal dimension of that concealment with a $5 million penalty — a sum so disproportionate to the scale of the violation that it functioned less as a rebuke than as a rounding error on a single afternoon’s investment returns. The legal ledger, by the institution’s own accounting, has been cleared.

By virtually any measure, the Church of Jesus Christ of Latter-day Saints is the wealthiest religious institution in the United States and among the wealthiest on earth — a position achieved in large part through a culture of tithing compliance forged in the nineteenth century and an investment operation that functioned, for more than twenty years, in deliberate concealment from both its members and federal regulators. The SEC settlement of 2023 addressed the legal dimension of that concealment with a $5 million penalty — a sum so disproportionate to the scale of the violation that it functioned less as a rebuke than as a rounding error on a single afternoon’s investment returns. The legal ledger, by the institution’s own accounting, has been cleared.

But the spiritual ledger has never been opened. The Church issued no formal apology to its members for the concealment. No General Authority stood at a General Conference pulpit and acknowledged that the men and women who had faithfully dropped their envelopes into the clerk’s hands every week — the widow in rural Mexico, the retiree on a fixed income, the young family stretching a budget to honor their covenant — had been deliberately kept from knowing that their contributions were not needed in the way they had been led to believe. No accounting was offered of how the decision to conceal was made, who authorized it, and what spiritual authority was invoked to justify deceiving the very people whose covenant faithfulness had built the reserve in the first place. The institution that claims prophetic leadership, that presents tithing as a sacred covenant with eternal consequences, and that requires its members to demonstrate personal worthiness in a bishop’s interview before entering the house of the Lord — that institution treated the discovery of its twenty-year financial concealment as a compliance matter to be settled, not a betrayal to be confessed. In the vocabulary of the faith it professes, there is a word for receiving another person’s sacrifice under false pretenses. That word has not yet been spoken.

Section Two: What Does the Bible Say? The Theology of Wealth, Stewardship, and Giving

God Owns Everything: The Foundational Premise

Any serious biblical engagement with the question of institutional wealth must begin where Scripture itself begins: with the declaration that God is the absolute owner of all things. “The earth is the Lord’s, and all its fullness, the world and those who dwell therein” (Psalm 24:1). This is not a peripheral text; it is the foundation of the entire biblical theology of stewardship — articulated by the Reformed theologian R.C. Sproul in a reflection that remains standard in evangelical theological education.

“God is the author of all things, the Creator of all things, and the owner of all things. Whatever God makes, He owns. What we own, we own as stewards who have been given gifts from God Himself. God has the ultimate ownership of all of our ‘possessions.’ He has loaned these things to us and expects us to manage them in a way that will honor and glorify Him.” — R.C. Sproul, “What Does the Bible Say About Christian Tithing?“ Ligonier Ministries

It is worth pausing here to acknowledge a persistent LDS hermeneutical defense. When confronted with biblical texts that challenge Latter-day Saint doctrine or practice, the Church and its apologists frequently retreat to the Eighth Article of Faith, which holds that the Bible is the word of God only “as far as it is translated correctly” — a carefully constructed qualifier that allows virtually any inconvenient passage to be set aside as corrupted in transmission. It is a theologically elegant escape hatch.

But that defense crumbles under the weight of two centuries of serious scriptural exegesis. Psalm 24:1, cited above, is not a disputed translation. It appears with remarkable consistency across the Septuagint, the Masoretic Text, the Latin Vulgate, the King James Version, and every major modern translation. No credible textual scholar has identified it as a corruption. The same is true of the New Testament passages most directly relevant to wealth, accumulation, and the obligations of the powerful toward the poor. The LDS “translation” qualifier was never intended — and cannot honestly be deployed — as a universal solvent to dissolve every biblical challenge to institutional behavior. When the manuscript tradition is unified, when the exegetical consensus is clear, and when the plain meaning of the text is unmistakable, the defense of mistranslation is not a scholarly argument. It is an evasion.

But that defense crumbles under the weight of two centuries of serious scriptural exegesis. Psalm 24:1, cited above, is not a disputed translation. It appears with remarkable consistency across the Septuagint, the Masoretic Text, the Latin Vulgate, the King James Version, and every major modern translation. No credible textual scholar has identified it as a corruption. The same is true of the New Testament passages most directly relevant to wealth, accumulation, and the obligations of the powerful toward the poor. The LDS “translation” qualifier was never intended — and cannot honestly be deployed — as a universal solvent to dissolve every biblical challenge to institutional behavior. When the manuscript tradition is unified, when the exegetical consensus is clear, and when the plain meaning of the text is unmistakable, the defense of mistranslation is not a scholarly argument. It is an evasion.

What remains, then, is the text itself — and the text is unambiguous. God owns everything. Human beings, institutions included, are stewards — not proprietors. That distinction carries profound implications for how a religious institution ought to hold, deploy, and account for the resources entrusted to it in the name of the faithful.

The implication of divine ownership is profound. If an institution that claims to represent God’s kingdom on earth accumulates wealth without accountability, without transparency, and without evident alignment with God’s stated priorities — particularly care for the poor — it is not merely guilty of poor management. It is guilty of unfaithfulness as a steward.

Old Testament Foundations: Tithing and Its Context

The tithe — from the Hebrew ma’aser, meaning “tenth” — appears first in Genesis 14, where Abraham gives a tenth of the spoils of battle to Melchizedek, the enigmatic priest-king of Salem who receives him after his victory over the kings of the east (Genesis 14:18–20). It is the earliest recorded act of tithing in Scripture, predating the Mosaic law by centuries, and, significantly, it is entirely voluntary — prompted by gratitude, not commanded by statute. The tithe is later developed systematically in the Mosaic legislation: Leviticus 27:30–32 establishes the tithe as holy to the Lord; Numbers 18:21–29 designates it as provision for the Levitical priesthood; and Deuteronomy 14:22–29 elaborates a multi-component structure that is often flattened in popular Christian usage. The prophet Malachi issues the most famous tithing exhortation in all of Scripture — “Bring the whole tithe into the storehouse, that there may be food in my house” (Malachi 3:10) — in the context of a post-exilic community that had grown negligent in its covenantal obligations.

Several features of the Old Testament tithe deserve careful attention. First, the system was not monolithic. Hebrew scholarship and the rabbinic tradition identify at least two and arguably three distinct tithes in the Mosaic law: the Levitical tithe supporting the priestly class (Numbers 18), a festival tithe supporting communal worship and celebration (Deuteronomy 14:22–26), and a poor tithe collected every third year specifically for the widow, the orphan, the resident foreigner, and the destitute (Deuteronomy 14:28–29). The poor tithe alone undermines any reading of biblical tithing as a simple institutional funding mechanism. It was structurally designed, from its inception, to serve the most vulnerable members of the covenant community.

Second, the theological logic of the tithe ran from gift to gratitude — not from payment to blessing. The Mosaic tithe was a response to God’s prior provision, an acknowledgment of dependence, and an act of covenant fidelity. The prosperity-theology inversion — in which withholding the tithe “robs God” and paying it functions as a transactional key to divine favor — represents a significant distortion of the original Mosaic intent. It reframes an act of worship as a financial instrument, and theologians across Catholic, Reformed, and mainline Protestant traditions have identified this as a departure from both the text and its context. The Malachi passage itself, so frequently deployed in LDS tithing instruction, is addressed to a specific covenant community in a specific moment of national unfaithfulness — not to a universal principle of spiritual economics.

Second, the theological logic of the tithe ran from gift to gratitude — not from payment to blessing. The Mosaic tithe was a response to God’s prior provision, an acknowledgment of dependence, and an act of covenant fidelity. The prosperity-theology inversion — in which withholding the tithe “robs God” and paying it functions as a transactional key to divine favor — represents a significant distortion of the original Mosaic intent. It reframes an act of worship as a financial instrument, and theologians across Catholic, Reformed, and mainline Protestant traditions have identified this as a departure from both the text and its context. The Malachi passage itself, so frequently deployed in LDS tithing instruction, is addressed to a specific covenant community in a specific moment of national unfaithfulness — not to a universal principle of spiritual economics.

Third, the entire tithe system presupposed transparency and communal accountability. Ancient Israel’s priestly apparatus operated within a covenant community that could, in principle, observe how the tithes were received and distributed. The storehouse of Malachi was not a private investment vehicle. It was a public institution whose stated purpose — “that there may be food in my house” — was tangible, verifiable, and oriented toward the sustenance of the priestly community and the relief of the poor. There was no equivalent of Ensign Peak Advisors. There was no secretive investment arm accumulating surplus in amounts that dwarfed the entire functioning budget of the religious establishment — no shell companies, no lifetime confidentiality agreements, no opaque portfolio shielded from the very people whose covenant faithfulness had funded it. The storehouse was visible. The need was real. The purpose was declared. On all three counts, the contrast with modern LDS institutional finance could hardly be more stark.

The New Testament: Jesus, Generosity, and the Danger of Wealth

Jesus spoke about money more than almost any other topic in the Gospels — more than prayer, more than baptism, more than the Sabbath. His teachings consistently and emphatically warn against the accumulation of wealth as an end in itself, and consistently prioritize the poor, the marginalized, and the vulnerable.

The theological meaning of the Widow’s Mite (Mark 12:41-44; Luke 21:1-4) is particularly striking in light of the LDS financial situation. Jesus observes wealthy donors contributing large sums to the Temple treasury, then watches a poor widow deposit two small copper coins. His commendation of her is unambiguous: “Truly I tell you, this poor widow has put in more than all of them. For they all contributed out of their abundance, but she, out of her poverty, put in all she had to live on.” (Mark 12:43-44; Luke 21:3-2).

What Jesus does not say is equally instructive. He does not instruct the Temple authorities to refund her offering. He does not condemn the act of giving, nor does He intervene to relieve her of her obligation. The institution receives what she brings, and He permits it. But the irony of the passage — that the very Temple system He is observing would be reduced to rubble within a generation (Luke 21:5–6), its stones thrown down, its religious economy utterly dissolved — suggests something far more searching than a simple commendation of generosity. Jesus watches a poor woman give everything she has to an institution that He knows is living on borrowed time. He praises her faith. He does not praise the institution that accepted it. The passage is not merely a portrait of sacrificial giving. Read in its full Lukan context, it is a warning about what religious institutions become when they lose sight of the people they were built to serve — when the Temple that was meant to be a house of prayer for all nations becomes, instead, a financial apparatus that receives the widow’s last coin and builds nothing for her with it. The commendation belongs to her. The indictment belongs to the temple. That distinction is not incidental. It is the whole point.

“The Mosaic tithe was not a means of climbing the ladder to God’s favor; it was a response to grace already received… Jesus pressed the principle deeper still: joyful, uncalculating generosity as the natural expression of a heart already transformed by the gospel.” — Ray Ortlund, “Jesus and Tithing,” The Gospel Coalition

The Apostle James delivers perhaps the most direct biblical warning against the hoarding of wealth. In James 5:1-6, he writes with striking severity: “Come now, you rich, weep and howl for the miseries that are coming upon you. Your riches have rotted, and your garments are moth-eaten. Your gold and silver have corroded, and their corrosion will be evidence against you and will eat your flesh like fire. You have laid up treasure in the last days.” Whatever the doctrinal differences between traditional Christianity and the LDS Church, this text speaks across those differences with equal force.

Christian Consensus on Wealth and Stewardship

Across the breadth of Christian theological tradition — Catholic, Orthodox, Reformed, Methodist, Baptist, and Pentecostal — there exists a remarkable consensus on certain principles regarding wealth and its management by religious institutions. These include: the recognition of God’s ultimate ownership of all resources; the call to transparent, accountable stewardship; the priority of care for the poor; the danger of institutional wealth becoming self-perpetuating; and the requirement that financial practices align with the Gospel’s content.

“Biblical stewardship encompasses not only how we give but how we live — with honesty, accountability, and a consistent orientation toward the flourishing of the community, especially its weakest members. The Christian perspective is that wealth is neither inherently blessed nor inherently cursed, but it is always a test of the soul and the institution that holds it.” — Abundant Life Church, “Christian Perspective on Wealth and Poverty“

It is against this consensus that the LDS Church’s financial practices must be evaluated — and against which LDS apologists have attempted, with varying degrees of persuasiveness, to defend them.

Section Three: Tithing in the LDS Church — Doctrine, Compliance, and the Accusation of Hypocrisy

The LDS Theology of Tithing

Tithing in the Church of Jesus Christ of Latter-day Saints is not merely encouraged. It is, in practice, required — though the mechanism by which that requirement operates deserves careful examination.

To obtain a temple recommend, a member must meet with their bishop for a private interview. Among the standard questions is one regarding tithing: specifically, whether the member considers themselves a full-tithe payer. LDS leadership has been careful, at the institutional level, to define a “full tithe” as ten percent of one’s “increase” — a term deliberately left open to individual interpretation. General Authorities have occasionally acknowledged that members may prayerfully determine what “increase” means in their own circumstances. In that narrow sense, the Church does not formally mandate a mathematically precise ten percent of gross income from every member in every situation.

But that institutional nuance rarely survives the bishop’s office. In practice, the temple recommend interview creates a binary outcome — recommend granted or recommend withheld — and the implied assumption underlying the tithing question is a full ten percent. Few bishops probe the theological subtleties of increase with their congregants. Few members leave that interview believing that nine percent, or a tithe calculated on net rather than gross income, will satisfy the requirement. The ambient teaching — reinforced across decades of General Conference addresses, Sunday School curriculum, and youth instruction — is clear: ten percent, paid consistently, is what faithfulness looks like. The doctrinal flexibility exists on paper. The social and ecclesiastical pressure points in only one direction.

The stakes of that pressure are not trivial. In LDS theology, the temple endowment and the sealing ordinance are not optional enhancements to salvation — they are prerequisites for exaltation in the Celestial Kingdom, the highest of three degrees of glory in the LDS afterlife. The other two — the Terrestrial and Telestial Kingdoms — represent lesser degrees of eternal reward, reserved for those who were honorable but not fully faithful, or who rejected the gospel altogether. Only the Celestial Kingdom offers what LDS theology calls exaltation: eternal progression, the presence of God the Father, and the continuation of the family unit throughout eternity. It is not merely the preferred destination. Within the believing Latter-day Saints’ framework, it is the only destination that fulfills the entire purpose of mortal life, and access to it runs directly through the temple recommend that a full tithe makes possible.

A member who cannot obtain a temple recommend is not merely inconvenienced; they are, by the internal logic of LDS doctrine, excluded from the highest eternal reward their faith offers. Without a valid recommend, a member cannot receive their own endowment, cannot be sealed to a spouse for “time and all eternity,” cannot participate in proxy ordinances for deceased ancestors, and cannot attend their own child’s temple wedding ceremony — watching from outside while the sealing proceeds within. The theology is explicit: ordinances performed in the temple are binding in eternity in ways that no other ceremony, however sincere, can replicate. To be barred from the temple is, in the most consequential sense, what LDS doctrine recognizes to have one’s ultimate eternal trajectory placed in jeopardy.

The requirement to tithe stands, therefore, at the threshold of eternity — not merely at the door of a building. It may be softly worded at the institutional level, framed in the language of personal worthiness and prayerful discernment. But at the level of lived experience, in the quiet of a bishop’s office where a recommend is either signed or withheld, it functions as an absolute — one with consequences that, in the believing member’s understanding, extend not just through this life, but through all lives to come.

This is an extraordinary institutional mechanism — and it is documented in the Church’s own official sources. The General Handbook of the Church of Jesus Christ of Latter-day Saints is a sprawling administrative document governing virtually every dimension of member life: who may be baptized and under what conditions, how ordinances may be recorded and validated, when a civil marriage may be performed and by whom, how a patriarchal blessing may be replaced, what constitutes grounds for a membership council, and hundreds of additional regulatory provisions that govern the lived experience of 17.5 million members from cradle to grave. It is, in its scope and granularity, a document the Jewish Pharisees would have recognized — and perhaps admired. The Pharisaic oral law, known as Halachah, was itself an attempt to build a protective fence of regulatory precision around the Torah, interpreting and extending the written commandments into every corner of daily life. The rabbis counted 613 commandments in the Mosaic law and proceeded to surround them with thousands of additional rulings.

The General Handbook operates in a recognizably similar spirit: where Scripture is silent or general, institutional policy fills the gap — exhaustively, hierarchically, and with an apparatus of interviews, approvals, and First Presidency exceptions that would not look out of place in a government bureaucracy. The analogy to secular regulatory complexity is not merely rhetorical. Consider the average American taxpayer confronting the United States Internal Revenue Code — a statutory document running between 6,000 and 7,500 pages of law as written by Congress. When federal tax regulations, IRS guidance documents, revenue rulings, and accumulated case law are added, the full body of material commonly referenced as “the tax code” expands to somewhere between 70,000 and 75,000 pages. No ordinary citizen is expected to have mastered it. Armies of credentialed professionals exist for no other reason than to navigate it on their behalf. The system is, by any honest assessment, a monument to institutional complexity that has long since outgrown its original purpose.

The General Handbook is not 75,000 pages. But it operates on the same institutional logic — the belief that every contingency must be anticipated, every exception governed, every edge case assigned to a procedural category — applied to the administration of a faith whose founder summarized the entirety of the law and the prophets in two commandments. By comparison, the Sermon on the Mount fits on two pages. The early church described in the Book of Acts fit in a borrowed upper room. What the General Handbook represents is not the elaboration of those beginnings. It is their institutionalization — the transformation of a living covenant into a managed compliance system, complete with its own exceptions, its own appeals process, and its own gatekeepers. The Pharisees, at least, were working without a word processor.

Within this framework, the tithing-temple recommend requirement is not an isolated rule. It is one node in a vast regulatory system in which access to the ordinances of salvation is mediated at every level by institutional compliance. The General Handbook lists full-tithe payment as a non-negotiable prerequisite for a temple recommend, with the local bishop serving as the sole arbiter. There is limited episcopal discretion in exceptional circumstances, but the structural requirement is unambiguous: no full tithe, no recommend; no recommend, no temple; no temple, no exaltation. A member who falls into financial hardship and cannot pay a full tithe becomes, within that framework, ineligible for the ordinances of salvation.

What makes this particularly difficult to dismiss as a technicality is that the Church’s own prophetic leadership has directly addressed the scenario — and resolved it in favor of tithing. In October 1998, President Gordon B. Hinckley visited Saints in Central America devastated by Hurricane Mitch, many of whom had lost their homes, their food, and their livelihoods. His counsel to them, delivered in person and later published in the official General Conference curriculum, was unambiguous: pay your tithing first, and the Lord will ensure you always have food on your table, clothing on your back, and a roof over your head. The theological logic echoes Elijah’s instruction to the widow of Zarephath — give first to God, and provision will follow. But Elijah was not simultaneously managing a $206 billion reserve fund. The institution delivering that counsel to hurricane survivors was.

The theological framing presented to members emphasizes faith, sacrifice, and covenant. President Gordon B. Hinckley, a beloved twentieth-century Church president, described tithing as “a principle of promise, of prosperity, of blessing, and of great consequence.” Church leaders commonly cite Malachi 3:10 to argue that tithing is a divine financial law with promised material rewards for obedience.

“Tithing is a fundamental doctrine in The Church of Jesus Christ of Latter-day Saints, requiring members to contribute 10% of their income to the Church. It is framed as a commandment from God, essential for spiritual growth, obedience, and blessings. Paying a full tithe is also a requirement for temple access, making it a key factor in a member’s ability to participate in sacred ordinances, including those necessary for eternal salvation.” — WasMormon.org, “Tithing is About Money, Not Faith, Obedience, Loyalty, or Sacrifice“

The Temple Recommend and Financial Coercion: A Critical Analysis

The practice of making temple access contingent upon tithing compliance is, from a traditional Christian perspective, deeply problematic. The New Testament’s consistent teaching is that access to the covenant community, to worship, and to the Lord’s Supper is not conditional upon financial giving. Jesus drove the money changers from the Temple precisely because financial transactions had become a barrier to worship (John 2:13-17). The early church explicitly rejected any system in which material standing determined spiritual standing.

The LDS system also generates a troubling dynamic of coercive pressure. When institutional leadership knows that investment returns are sufficient to fund all operations indefinitely — and withholds that information from members to maintain tithing compliance — the ethical dimension becomes unmistakable. As Roger Clarke, Ensign Peak’s director, acknowledged to the Wall Street Journal, the Church concealed its reserves specifically because it feared members would reduce their giving if they understood the Church did not need the money.

This admission cuts to the heart of the hypocrisy charge. LDS leaders have consistently framed tithing in the language of sacrifice, covenant, and spiritual obligation. Members in poverty have been encouraged — and in the case of temple access, required — to give ten percent of income to an institution that, by its own financial leadership’s admission, was hiding the fact that it did not need their money. The theological language of sacrifice was deployed in the service of financial accumulation.

“They [Church leaders] use coercive rhetoric to pressure members into financial obedience while sidestepping the vast wealth the Church has amassed. They are doing their best to make this money commandment to be associated with anything but money.” — WasMormon.org, “Tithing is About Money, Not Faith, Obedience, Loyalty, or Sacrifice“

It is worth clarifying what traditional Christian theology does and does not say here. The practice of giving — indeed, of sacrificial giving — is fully affirmed in the New Testament. Paul’s letters celebrate the generosity of impoverished Macedonian churches (2 Corinthians 8:1-5). The principle of proportional giving is present in both Testaments. The critique is not that tithing is wrong. The critique is that a $293 billion institution continues to require financial compliance from its poorest members while concealing from them information that would be material to their decision about how much to give.

Charitable Giving in Context: A Question of Proportion

When discussing LDS charitable activities, it is important to be precise. The Church reported spending $1.45 billion in humanitarian assistance in 2024, up from $1.3 billion the year before — figures the Salt Lake Tribune characterized as a genuine and notable increase. The Church also operates an extensive welfare system, funds global missionary work, maintains three university systems (including Brigham Young University), and provides considerable social infrastructure for its members worldwide.

However, context matters profoundly. If the Church’s investment portfolio generates returns in the range of $23.5 billion in a single year (as estimated by The Widow’s Mite Report for 2024), then $1.45 billion in humanitarian aid represents approximately 6.2 percent of investment returns in that year alone — and a far smaller fraction of total accumulated wealth. The Church receives an estimated $5.5 to $6.5 billion annually in member tithing. It gives back roughly one-quarter to one-fifth of that in humanitarian assistance.

The University of Virginia’s Mormon Studies program, in a nuanced 2019 analysis, noted that the LDS Church’s centralized financial model means it bears costs other denominations distribute locally — construction, utilities, and program costs for over 30,000 congregations worldwide. This is a legitimate observation, and it qualifies simple comparisons. But even accounting for these substantial operational costs, the accumulation of a $206 billion investment reserve — growing faster than it can be spent, designed by its own custodians to be permanent and self-sustaining — raises questions that institutional efficiency arguments cannot answer.

“The church has centralized the payment of all expenses associated with membership, regardless of the amount of member contributions. All such contributions are wire transferred to headquarters and distributed globally… So much more could be said.” — University of Virginia Mormon Studies, “Mormonism and its Money.”

Local Meetinghouse Construction and Expenses

Local LDS ward and meetinghouse funding operates through a centralized system that has evolved significantly over the Church’s history — and its structure carries significant implications for any discussion of tithing and institutional wealth.

Meetinghouse Construction. All meetinghouse construction costs are funded entirely by the Church’s central headquarters in Salt Lake City, drawn from general tithing revenues. Local congregations bear none of the capital construction cost. The Church uses standardized floor plans worldwide to reduce building expenses by as much as 20%, with local architects hired to execute those plans. Notably, approval for a new meetinghouse has historically required a prescribed percentage of adult members in the congregation to be full-tithe payers — meaning tithing compliance is not just a funding source but a gatekeeping criterion for whether a ward even receives a building.

Local Operational Expenses. Since January 1, 1990, ward and stake operational expenses in the United States and Canada have been funded entirely through a budget allowance program — a quarterly allocation of general Church funds sent directly from Salt Lake City to each unit. The First Presidency’s letter announcing the change explicitly credited “the faithfulness of members in paying tithing” as having made this possible. Under this system:

• All activities, programs, manuals, and supplies are paid from the central allocation.

• Members are explicitly told they should not pay fees or personally supply materials for Church activities.

• Building utilities, maintenance, telephones, and computers are paid separately from general Church funds, outside the local budget.

• Local tithing collected in a ward is forwarded entirely to Salt Lake City — the ward retains none of it.

What This Means in Context. The financial architecture is revealing — and members with access to ward financial records have documented it in striking detail. A 2020 Reddit post sharing an actual ward budget illustrated the asymmetry with clinical precision: in 2019, that single ward forwarded $490,000 in tithing to Salt Lake City — down from $560,000 the prior year — while operating on a local budget of approximately $10,500. Fast offerings collected locally were largely sent to headquarters as well, with only a fraction retained for local needs. The ward’s budget allocation represented less than two percent of the tithing it generated.

This is not an isolated case. Across dozens of member accounts, the pattern is consistent and quantifiable. One former ward clerk reported that his ward collected $675,000 in tithing from roughly 100 active adults and received back a ward budget of $6,200. Another ward with 200 weekly attendees forwarded an estimated $900,000 to Salt Lake while operating on an $8,000 budget. A third account described weekly tithing receipts running in the thousands of dollars against an annual activity budget measured in the hundreds. One commenter summarized what many clerks eventually discover: “If ward budget is over 1% of tithing collected, I would be shocked”.

The bishop collects the envelopes, forwards every dollar to Salt Lake City, and waits for a quarterly disbursement that will not cover a youth camp, let alone the spiritual weight of what those envelopes represent to the people who sealed them. The building those members meet in, the utilities that keep the lights on, and the maintenance that keeps the carpets clean are paid separately — directly by headquarters — from centralized funds whose total scale, investment returns, and distribution rationale remain entirely undisclosed to the same members whose covenant faithfulness generated them. The ward is, in effect, a tithing collection point for an institution whose financial operations its members are not permitted to examine. The widow drops in her thirty-five cents. It travels to Salt Lake City. And there the accounting ends — for her.

Section Four: The Apologists’ Defense — FAIR, Jeff Lindsay, and the Limits of Institutional Justification

The FAIR Latter-day Saints Response

FAIR Latter-day Saints — formerly FairMormon — is one of the principal apologist organizations defending LDS theological and institutional practices. When the Wall Street Journal’s 2020 investigation broke the Ensign Peak story, FAIR published a response by volunteer Sarah Quan acknowledging the legitimacy of questions while defending the Church’s approach on four grounds:

First, FAIR argued that the principle of self-reliance counsels against massive direct aid programs, citing concerns about creating dependency and harming local economies. Second, it invoked the sacred nature of tithing funds — that the Church’s extreme caution in how it spends donations reflects appropriate stewardship. Third, it noted the Church’s substantial non-monetary contributions (volunteer labor, in-kind assistance). Fourth, it pointed to a lack of public information sufficient to render a definitive judgment.

“Frankly, we don’t know enough about Ensign Peak as a general populace to really say one way or another. The issue is nuanced, and a single whistleblower report is not enough for us to draw a good conclusion about the church’s financial situation or intentions.” — FAIR Latter-day Saints (FairMormon), “Is the Church Excessively ‘Hoarding’ Money?“

The appeal to insufficient information is notable. It was made in 2020, before the SEC action confirmed that the shell-company structure was indeed designed to conceal the portfolio’s size. It was made before The Widow’s Mite Report’s sophisticated modeling confirmed that the fund had surpassed $200 billion. The “we don’t know enough” argument was, in retrospect, not a call for epistemological humility but a holding action against scrutiny that subsequent events have rendered untenable.

The self-reliance argument has more merit at a philosophical level, but ultimately fails the proportionality test. The concern that direct aid creates dependency is a legitimate point debated among international development scholars. But it does not explain why investment reserves should grow to $206 billion rather than, say, $20 billion — a sum that would still provide an extraordinarily robust buffer against economic downturns while releasing enormous resources for charitable deployment. The doctrine of self-reliance does not require hoarding.

Jeff Lindsay and the Financial Empire Defense

Jeff Lindsay, a prominent LDS apologist, offers a more comprehensive defense of the Church’s financial practices on his website. Lindsay’s argument centers on the claim that the Church’s financial goals are genuinely mission-driven: that investments fund temples, missionary work, education, and welfare worldwide; that Church leaders live modest lives without personal enrichment; and that the global scale of the Church’s operations necessitates substantial reserves.

“The motives at the core of the Church, which affect what it does at the local, regional, national, and global level, from top to bottom, are not about personal gain. They are not about glory and power, comfort and ease, or living exorbitant lifestyles. The focus and primary goals that motivate actions and decisions are not desires for individual gain, but the desire to bless the world.” — Jeff Lindsay, “LDS FAQ: The Church and Its Money.”

Unlike the prosperity gospel preachers of American Evangelicalism, LDS general authorities do not publicly display extraordinary personal wealth. The Church’s Presiding Bishopric and apostolic leadership receive what officials describe as modest living stipends rather than executive-level compensation packages. On its face, this is a legitimate and meaningful distinguishing feature — and it deserves acknowledgment.

But the full picture is considerably more complicated. The men called to serve as apostles, and General Authorities are not, as a rule, drawn from the ranks of schoolteachers, tradesmen, or subsistence farmers. They are drawn overwhelmingly from the upper tiers of American professional and commercial life — attorneys, corporate executives, university presidents, successful entrepreneurs, and career ecclesiastical administrators who spent decades building personal wealth before their calls to full-time Church service. Dallin H. Oaks was a Utah Supreme Court Justice and the president of Brigham Young University. Dieter F. Uchtdorf was a senior executive at Lufthansa. M. Russell Ballard came from a family of prominent Utah business leaders. Jeffrey R. Holland served as BYU president. The pattern is not incidental — it reflects a consistent institutional preference for leaders who arrive at the apostleship already financially secure, already embedded in elite professional networks, and already accustomed to the exercise of institutional authority.

The living stipend, in this context, is not quite the gesture of apostolic simplicity it appears to be. A man who enters full-time Church service with a seven-figure net worth, a paid-off home, and a lifetime of accumulated professional assets does not experience a modest stipend the way a rural convert in the developing world would experience one. The personal austerity is real, in its way. But it is the austerity of men who do not need the money, which is a rather different thing from the sacrificial simplicity of the New Testament apostles who left their nets on the shore of Galilee and followed with nothing.

Lindsay’s argument conflates the personal conduct of leaders with the institutional conduct of the organization. A leader can live humbly while stewarding an institution whose financial behavior raises profound ethical questions. The absence of personal greed does not address the structural question of why a religious institution accumulates investment reserves sufficient to fund itself forever, while simultaneously requiring the poorest members to tithe as a condition of their most sacred religious participation.

Lindsay also addresses the City Creek Center mall controversy by noting that Church officials confirmed no illegal activity was involved. This is technically accurate but misses the theological question. The use of tithing-derived investment funds to build a luxury commercial mall in downtown Salt Lake City — one that features high-end retail stores inconsistent with the Church’s own teachings on modesty and conspicuous consumption — is not rendered spiritually appropriate by its legal permissibility.

The “Rainy Day Fund” Defense and Its Limits

Church officials and their defenders have consistently described the Ensign Peak reserves as a “rainy-day account” — a prudent reserve against economic catastrophe that would allow the Church to continue its global mission even through severe financial crises. Christopher Waddell, second counselor in the Presiding Bishopric, told the Wall Street Journal: “If something like that [an economic recession] were to happen again, we won’t have to stop missionary work.”

This argument has genuine theological resonance with principles of provident living and preparation that the Church legitimately emphasizes. It also has some historical grounding: the Church’s near-bankruptcy in the 1890s was a formative institutional trauma that shaped subsequent generations of leadership.

But the rainy-day defense, taken seriously, generates its own critique. How large a rainy-day fund is sufficient? If investment returns now exceed annual operational costs — if, as The Widow’s Mite Report calculates, the fund could sustain the Church indefinitely even if all member contributions stopped — what weather event would justify a further $23.5 billion annual accumulation? And when, precisely, does a rainy-day fund become an end in itself?

Scripture does not condemn prudent saving. But neither does it commend indefinite accumulation at the expense of present generosity. “Do not store up for yourselves treasures on earth… but store up for yourselves treasures in heaven” (Matthew 6:19-20) is not merely personal financial advice. It is a structural critique of any institution — ecclesiastical or otherwise — that mistakes the preservation of capital for the fulfillment of divine calling.

The Reddit Defense and Popular LDS Voices

In online forums and community spaces, many faithful Latter-day Saints have offered defenses that go beyond official apologetics. A frequently cited argument on platforms like Reddit’s r/mormon is that the Church’s financial resources represent generations of faithful sacrifice — that the accumulated wealth is, in a sense, the concretized devotion of millions of believers over nearly two centuries. To critique the wealth, on this view, is to dishonor the sacrifice.

This is an emotionally resonant argument, and it deserves a respectful response. The generations of faithful LDS members who paid their tithing deserve enormous admiration. The widow in Mexico and her counterparts throughout the developing world, who sacrifice real material comfort to support their faith community, are participating in something genuinely sacred. Their devotion is not in question.

But the accumulated wealth does not belong to them. It belongs to a corporation — formally organized as the Corporation of the President of the Church of Jesus Christ of Latter-day Saints — whose governance is not democratic, whose financial decisions are not transparent, and whose leadership is not accountable to the member body in any procedural sense. Honoring the sacrifice of contributing members requires, at minimum, that their contributions be used transparently for purposes they would endorse — purposes consistent with the Gospel’s clear priorities.

Section Five: A Theological Reckoning — What the Numbers Mean

The Widow’s Mite as Institutional Indictment

The name chosen by the independent financial watchdog that tracks LDS Church finances is not accidental. The Widow’s Mite Report deliberately invokes the passage in which Jesus commends the poorest giver and implicitly critiques the institution that receives her gift. For traditional Christians reading LDS finances through the lens of Scripture, the irony is pointed.

An institution that accumulates $293 billion, that earns more from investments than it spends on its entire global mission, that deliberately concealed this from members to prevent a reduction in donations, and that continues to require temple recommend compliance tied to tithing — including from its poorest members worldwide — faces a genuine theological reckoning with the words of Christ.

The problem is not merely one of public relations or institutional governance. It is a problem of theological integrity. The LDS Church professes a theology in which God is actively involved in directing the Church’s affairs through living prophets and apostles. If that claim is true, then the financial decisions of the institution are, in some meaningful sense, the decisions of a divinely directed organization. The question is, therefore, unavoidable: Does the God of the Bible — the God who made Himself known in the person of Jesus of Nazareth — direct a religious institution to accumulate $206 billion in investment reserves while asking widows for ten percent of their tortilla money?

The Biblical Standard Applied

Traditional Christian theology provides a clear framework for evaluating this question. The marks of faithful institutional stewardship in Scripture include transparency (Luke 16:10-12), proportionality (2 Corinthians 9:7-8), prioritization of the poor (Matthew 25:31-46), and accountability to the covenant community (Acts 4:34-35; 6:1-4). The early Jerusalem church, the standard New Testament model of communal economics, distributed “to each as any had need” — not to a permanent investment endowment.

Against these standards — divine ownership, structural provision for the poor, transparency, and the theological logic of gift rather than transaction — the LDS financial model presents a genuinely mixed picture. And that complexity deserves honest acknowledgment, not rhetorical convenience.

The Church does real good in the world. It operates welfare farms and maintains a network of bishops’ storehouses that provide food, clothing, and necessities to struggling members without bureaucratic means-testing. It funds a global missionary program that communities in the developing world often experience as genuinely transformative — providing not only religious instruction but social connection, literacy, and a sense of belonging that can be especially powerful in contexts of poverty and isolation. In recent years, the Church has increased its reported humanitarian expenditures, distributing aid across dozens of countries in response to natural disasters, refugee crises, and chronic poverty. These are real contributions. They represent real lives affected. They should not be dismissed, minimized, or treated as mere public relations.

But here a word of caution is warranted — one drawn not from secular criticism but from the lips of Jesus Himself. In Matthew 7:22, Christ warns of those who will appeal, on the day of final reckoning, to the breadth of their religious activity: “Many will say to Me in that day, ‘Lord, Lord, have we not prophesied in Thy name, and in Thy name cast out devils, and in Thy name done many wonderful works?‘” The warning is not directed at obvious hypocrites or avowed unbelievers. It is directed at those who have performed genuinely impressive religious works — and assumed those works were sufficient evidence of fidelity to God’s deeper requirements.

It is also worth noting that the humanitarian contributions the Church points to with justifiable pride do not occur in a vacuum. Organizations with no theological agenda whatsoever — Doctors Without Borders, the Bill & Melinda Gates Foundation, CARE International, World Vision, and the United Nations World Food Programme — collectively distribute tens of billions of dollars annually in direct humanitarian relief, with overhead ratios, audited financial statements, and programmatic accountability that are fully available to any donor who wishes to examine them. Doctors Without Borders publishes an annual report detailing every dollar received and spent. The Gates Foundation files detailed public disclosures as a matter of legal obligation and institutional culture. These organizations do not require their donors to demonstrate personal worthiness before a credentialing interview to contribute, nor do they withhold the benefits of their work from those who cannot afford to give.

It is also worth noting that the humanitarian contributions the Church points to with justifiable pride do not occur in a vacuum. Organizations with no theological agenda whatsoever — Doctors Without Borders, the Bill & Melinda Gates Foundation, CARE International, World Vision, and the United Nations World Food Programme — collectively distribute tens of billions of dollars annually in direct humanitarian relief, with overhead ratios, audited financial statements, and programmatic accountability that are fully available to any donor who wishes to examine them. Doctors Without Borders publishes an annual report detailing every dollar received and spent. The Gates Foundation files detailed public disclosures as a matter of legal obligation and institutional culture. These organizations do not require their donors to demonstrate personal worthiness before a credentialing interview to contribute, nor do they withhold the benefits of their work from those who cannot afford to give.

Charitable activity, however real, does not automatically sanctify the institutional structures that produce it. The question Scripture presses is not merely what was done, but in whose interest, with whose resources, under what terms of accountability, and with what transparency to those whose covenant faithfulness made it possible. A $293 billion institution that disbursed an estimated $906 million in humanitarian aid in 2023 — less than one-third of one percent of its total estimated wealth — while publishing no audited financial statements, maintaining no independent oversight, and conditioning its members’ eternal salvation on continued financial compliance, is an institution whose charitable works, however genuine, exist within a framework that the Matthew 7 warning was precisely designed to address.

The bishops’ storehouse is real. So is the $206 billion reserve that its donors were never told existed.

If rank-and-file Latter-day Saints are required to give a full tenth of their income to retain standing before God, one might reasonably ask why the institution’s own distribution of its vast investment returns falls well beneath that same threshold. The result is a distribution profoundly skewed toward institutional perpetuation and away from the biblical priority of the poor.

On the Question of Tax-Exemption

The Church of Jesus Christ of Latter-day Saints enjoys tax-exempt status under Section 501(c)(3) of the Internal Revenue Code — a designation it formally obtained from the IRS in 1941. This means that member tithing contributions are tax-deductible for the donor, and that investment returns generated by Ensign Peak’s estimated $206 billion in reserves are sheltered from federal income taxation. That is a substantial and ongoing public subsidy, underwritten by all American taxpayers regardless of their faith.

But the tax picture is considerably more complex — and more troubling — than the simple 501(c)(3) designation suggests. The Church operates a parallel commercial empire through Deseret Management Corporation (DMC), a for-profit holding company whose board of directors is drawn directly from the Church’s First Presidency and Quorum of the Twelve Apostles. DMC’s subsidiaries include Bonneville International (a major broadcasting company operating radio and television stations across the United States), the Deseret News, Deseret Book, and a portfolio of other revenue-generating enterprises. These are not charities. They are businesses competing in commercial markets alongside fully taxable corporations.